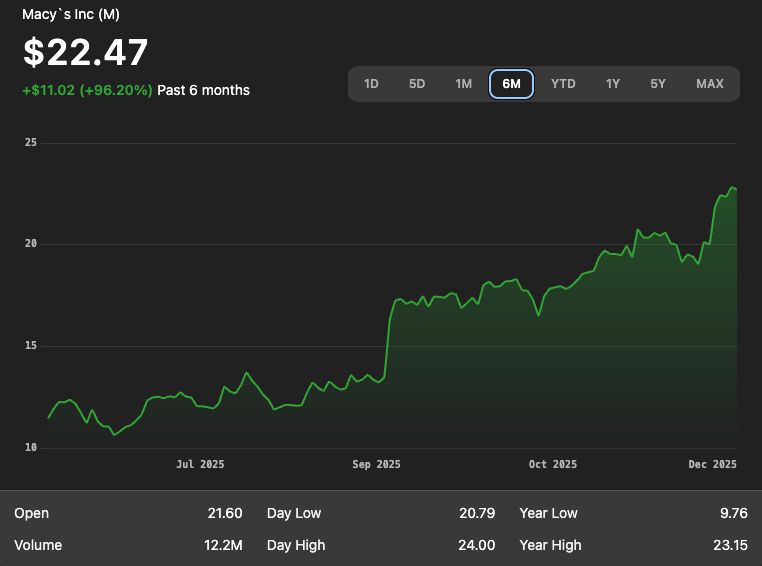

Q3 Results Surprise Wall Street

Macy's, Inc. delivered its third straight quarterly beat, reporting adjusted earnings of US $0.09 per share, far above analysts’ expectation of a loss. Revenue for the quarter reached approximately US $4.7 billion, also exceeding consensus estimates.

Comparable‑store sales rose by 2.5% year‑over‑year — the best result Macy’s has posted in over three years — signaling improvement under its ongoing turnaround efforts.

Upgraded Full‑Year Guidance

Buoyed by the stronger‑than-expected quarter, Macy’s raised its full‑year outlook. The company now expects adjusted EPS between US $2.00 and $2.20 (up from $1.70–$2.05) and net sales between US $21.48 billion and $21.63 billion (previously $21.15–$21.45 billion).

That upward revision reflects growing confidence in the company’s prospects — especially as it heads into the holiday season, a critical period for retail performance.

What's Driving the Turnaround

Macy’s is benefiting from a convergence of strategic moves, including store‑portfolio optimization, cost controls, and stronger demand within its core customer base.

A key factor: higher‑income shoppers have remained resilient even amid broader economic uncertainty, helping support sales especially in Macy’s higher‑end banners.

Also helping: leaner operating expenses — Macy’s achieved the EPS beat in part by cutting roughly US $40 million in SG&A costs.

The Road Ahead: Holiday & Beyond

With the company optimistic about the holiday shopping season, the updated guidance suggests Macy’s expects demand to hold up despite inflation pressures.

Still, some caution remains — Macy’s management acknowledges that consumers are becoming more selective in their spending, which could weigh on discretionary categories.

For Macy’s, the next few months will test whether this quarter’s momentum can translate into sustained performance — and whether the “Bold New Chapter” strategy truly marks a turning point.

{kind=link}